It happens every year — on the fifteenth day of the fifth month after the close of your nonprofit's fiscal year, to be exact.

That's right, I'm talking about nonprofits' annual return filing.

While nonprofit organizations are tax-exempt, they still have to submit forms (specifically the Form 990 series) to the IRS. As a nonprofit professional, you probably already know all of this information.

What you might not know, though, is the best way to fill out Form 990's statement of functional expense to accurately reflect your nonprofit's spending throughout the fiscal year.

That's likely because there are multiple methodologies you can use for functional expense allocation. And depending on the amount and type of funding your organization receives, your accounting department might rely solely on one method or a combination of all of them to complete your functional expense statement.

However, of these different methods, there's only one that — when done correctly — can help you monitor spending continuously, maximize funding, and even pass audits with flying colors: time studies.

To better understand functional expense allocation, time studies, and the connection between the two, let's take a closer look at both of these nonprofit terms.

What is Functional Expense Allocation?

Functional expense allocation is the process of describing how your nonprofit spends its money, required by IRS Form 990 and outlined by the Financial Accounting Standards Board (FASB)'s regulation ASU 2016-14. Under ASU 2016-14, nonprofits need to break expenses down into their functional and natural classifications.

Functional Classification

An expense can fall under one of three major functional classifications for a nonprofit.

Programs

Programs are the projects and activities that connect to your nonprofit's mission. Since furthering your mission is critical to your nonprofit's success, most of your expenses are likely program expenses. This can include expenses like program staff salaries, program supplies, or rent for program facilities.

Fundraising

To fund programs and keep your nonprofit running, you need to raise funds. Expenses related to fundraising activities could include creating and executing a marketing campaign to reach individual donors or holding an annual fundraising gala. If you have staff who dedicate all or most of their time to fundraising or donor outreach, their salaries will also be considered a fundraising expense.

Management and general

All other nonprofit expenses fall under the management and general function. You can think of these types of expenses as back office expenses that contribute to keeping your nonprofit up and running so you can execute on your programs. These could include expenses like general office supplies or salaries for staff (like your accountant) whose activities aren't always program-specific.

Natural Classification

An expense's natural classification gives even more detail about how your nonprofit's money was spent.

Natural classifications include many different types of expenses but can include classifications such as:

- Salaries and benefits

- Office supplies

- Rent for office space

- Utility bills

- Insurance

What Does a Functional Expense Statement Show?

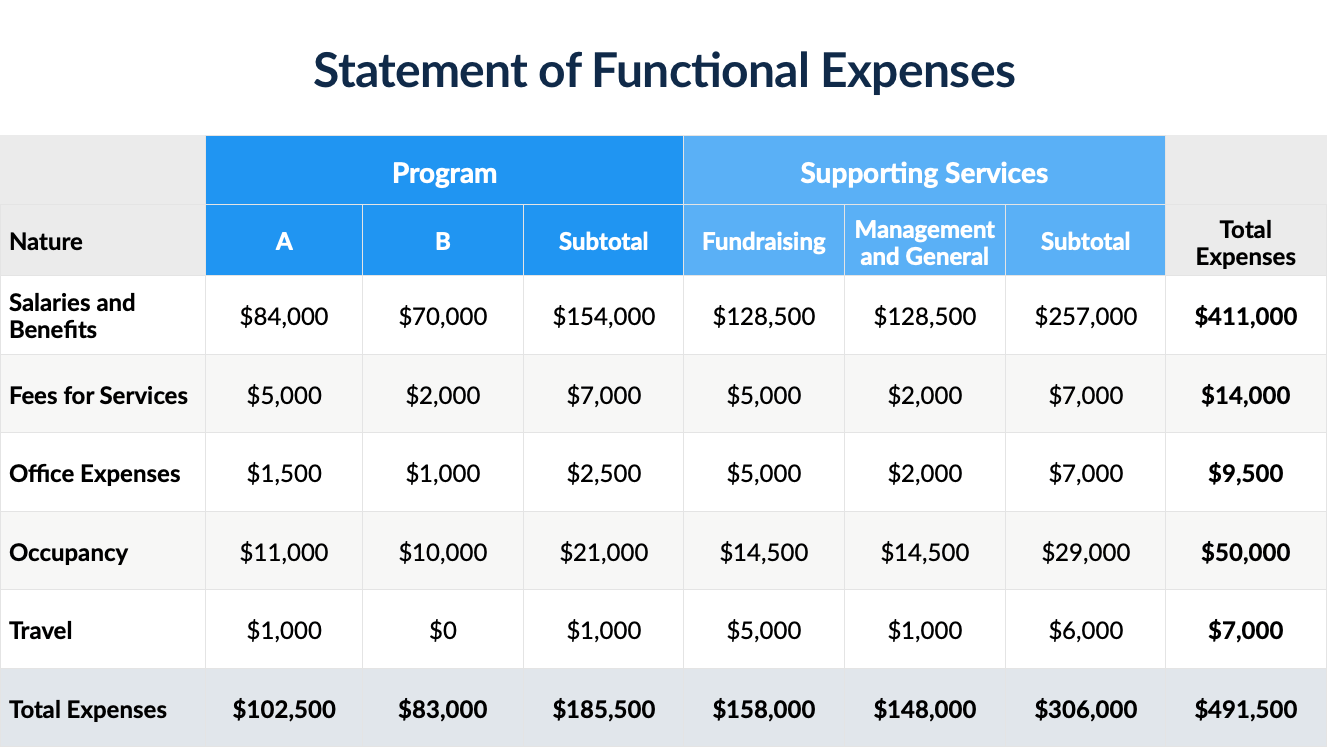

On a literal level, your nonprofit's functional expense statement shows all of your expenses with their functional and natural classifications.

So to file your statement of functional expenses, you might come up with a spreadsheet that looks something like this:

By dividing expenses this way, you can see how much you spent on each function, as well as on each natural classification.

Categorizing expenses this way is necessary for the IRS, but it's also important as a tool to answer an important question from funders: how much of their money goes directly toward programs.

Since programs directly contribute to furthering your nonprofit's mission, most funders — and the IRS — prefer that program expenses constitute the majority of your nonprofit's expenses. For funders, this is partially because it's much more exciting to say that they contributed to, say, helping to feed hungry children.

But for both funders and the IRS, lower overhead costs (typically not exceeding 35%) also show that your nonprofit is a responsible steward of its funding. Excessive overhead costs could indicate organizational bloat, misallocations of funding, and even fraud.

But how can you come up with these numbers to calculate the figures on your statement of functional expense, let alone compare your overhead and program costs?

Functional Expense Allocation Methods

There are several accepted methods you can use to come up with the numbers needed for your functional expense statement. You can mix and match these different methods to calculate the proportions spent on various functional expenses.

Direct

At first glance, the direct method of allocation seems like the most straightforward one. You allocate each expense to a functional category based on how the money was used. However, a quick examination shows that direct allocation isn't always possible.

Expenses like program materials are relatively easy to classify. For example, if you run an afterschool program and need to purchase 10 workbooks for it, you could allocate the costs of the workbooks directly to that program.

But outside of supplies and materials, many nonprofit expenses don't fit neatly into one functional classification. As we'll see when examining other allocation methods, many costs can — and should — be spread across different functional classes. For many nonprofit expenses, you'll have to use an indirect method of calculating and allocating costs.

Square Feet

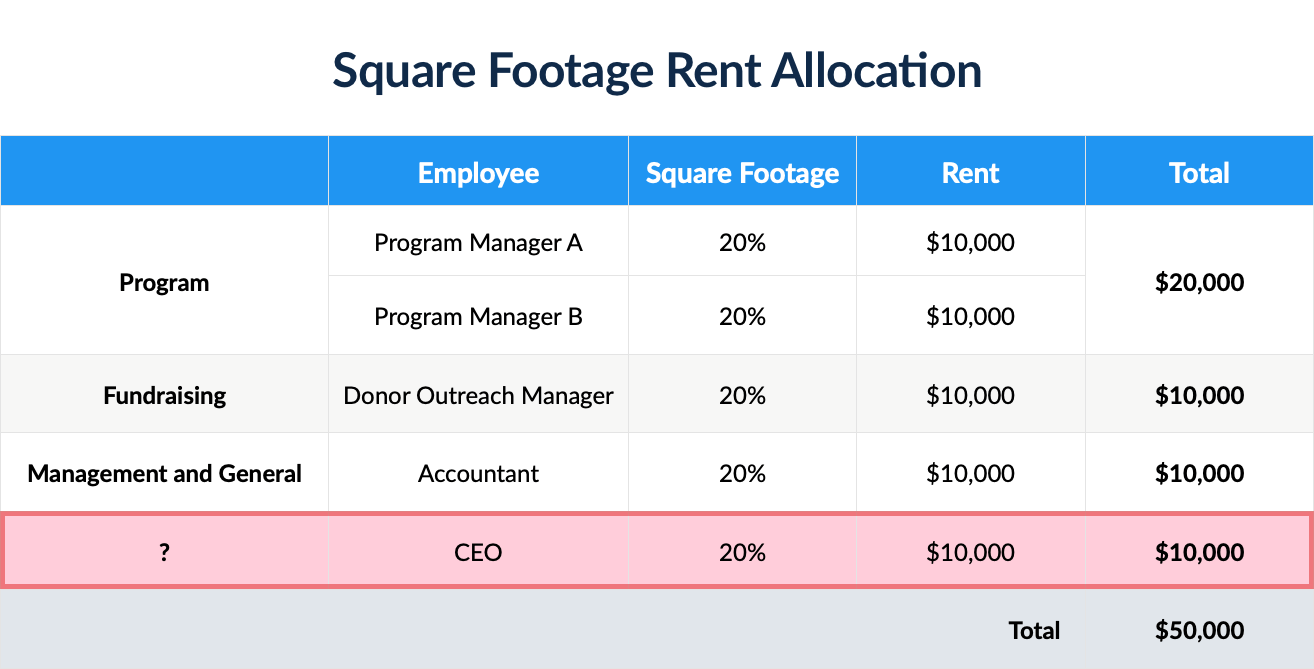

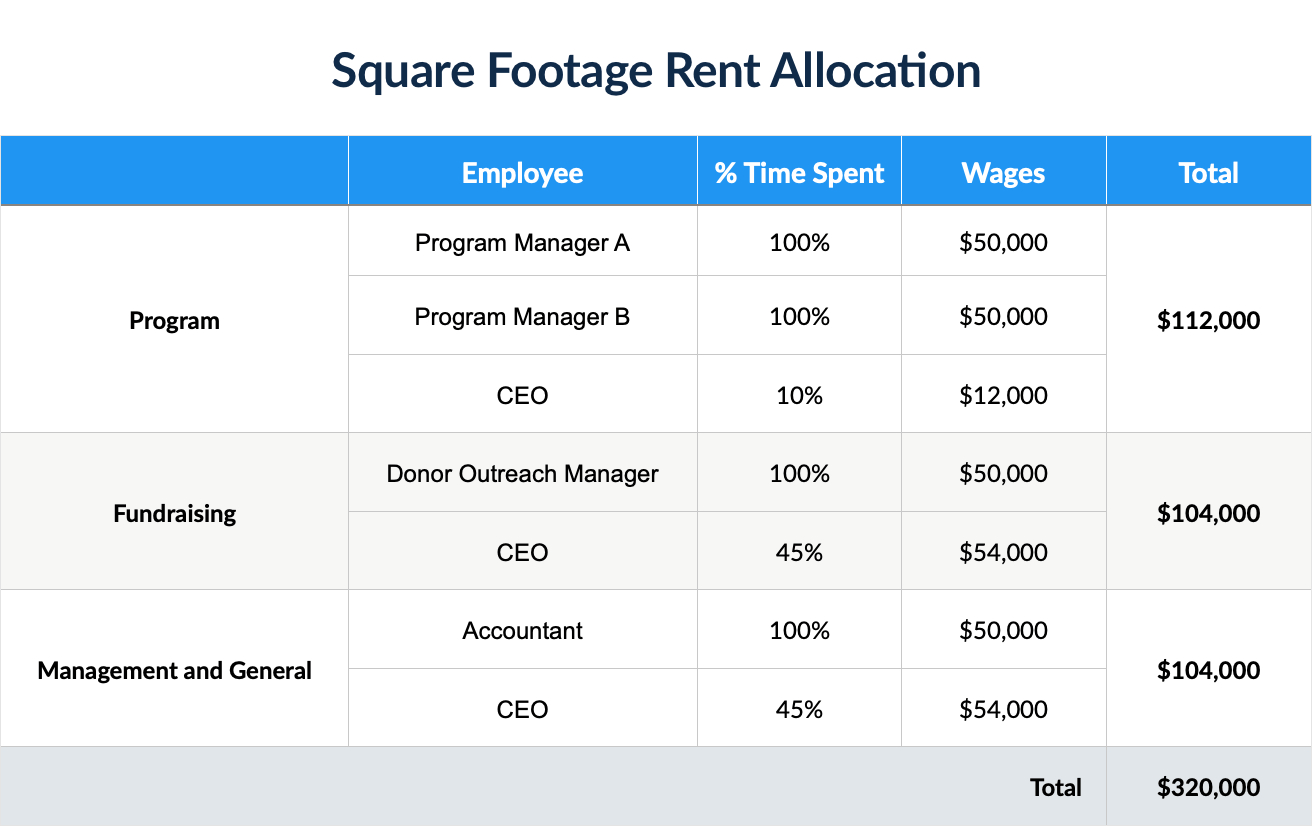

If you have a physical space like an office, you can allocate natural expenses like rent and utilities based on the amount of square footage each team takes up.

Let's say you have five employees. One works on Program A and another on Program B. You also have a donor outreach manager, an accountant, and a CEO. For the sake of simplicity, your office space is 1,000 square feet, and everyone's workspace takes up an equal amount of room (200 square feet, or 20% of the total office space). So you can divide your yearly rent (which we'll say is $50,000) by how much space everyone takes up.

That calculation would look something like this:

As you can see, the issue here is that someone like a nonprofit CEO, who wears many hats, might not fall easily into your program, fundraising, and management and general classifications. One way to reconcile these unallocated costs is to estimate where you think your CEO's duties fall.

Again, for the sake of simplicity, let's say you think your CEO's duties split evenly between fundraising and management and general activities. Using this estimate, you can allocate half of your CEO's square footage to fundraising, and the other half to management and general.

While using square footage of office space connects easily to certain expenses like rent, it doesn't always translate as easily to other types of expenses. And if you decided to go remote — after your experience during the COVID-19 pandemic, for example — you might not even have square footage to use as an allocating factor.

Headcount

Allocating expenses by headcount is another option for nonprofits, especially those without a dedicated office space.

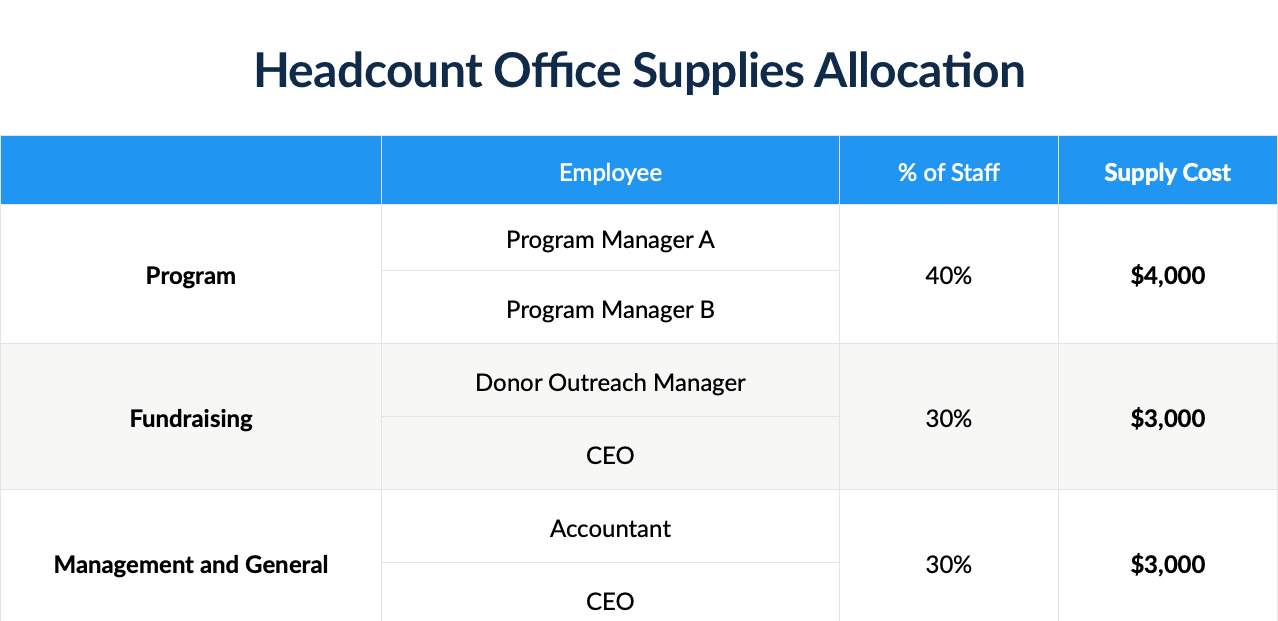

Let's continue with our example of a nonprofit with five employees. They've decided to get rid of their expensive office and work remotely. However, they now subsidize home office setups with the regular purchase and distribution of standard office supplies. This subsidy for their remote workforces adds up to $10,000 for the year.

Using the headcount method, you can divide costs by the number of employees working within each function. Again, we'll assume that the CEO divides her duties evenly between fundraising and management and general activities. That would look something like this:

The headcount method makes sense when allocating expenses like office supplies that are used by everyone in your organization. Especially if your organization is small, allocating these types of expenses by team or department size can help spread these costs over programmatic, fundraising, and management and general classifications.

But headcount, like square footage, relies on estimates like the one we used to decide how much of our expenses we can allocate to different functions based on the CEO's responsibilities. To allocate functional expenses with more accuracy and less guesswork, the best method is to look at employee timesheets.

Time Studies

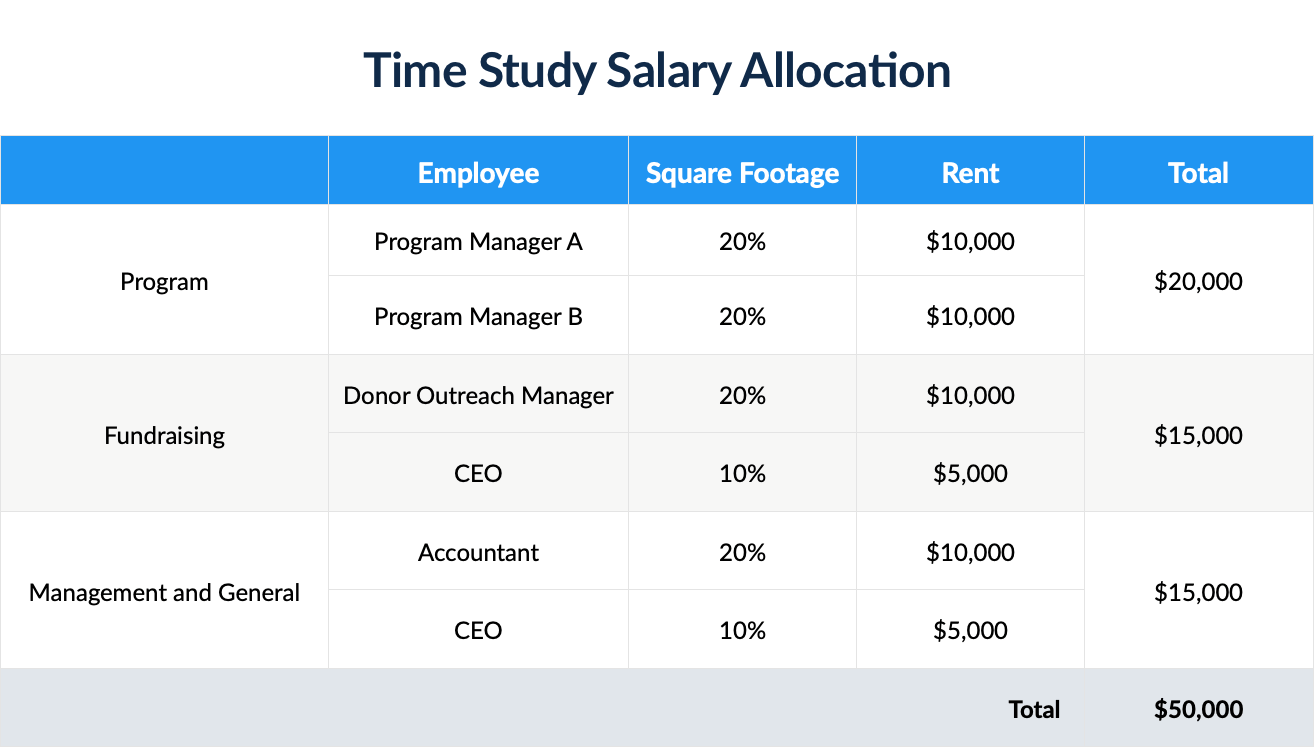

Time studies look at how employees spend their time to better understand where they should allocate certain expenses. Using data from employee timesheets helps you avoid the guessing and estimations that are part and parcel of the other allocation methods. And if done correctly, this data also helps solidify your allocation calculations if you ever have to defend them to an auditor.

For example, when using the square feet and headcount methods we made a guess about how to allocate rent and headcount expenses, respectively, based on what we assumed the CEO's role was. We might even have used some hard data to help us make that guess. Looking at the CEO's calendar, for example, we saw that in a given week, half her meetings were related to fundraising and half to general and administrative issues.

But when we use timesheets — and proportions of time spent working within various functions of a nonprofit organization — we can more accurately allocate expenses to their different functions.

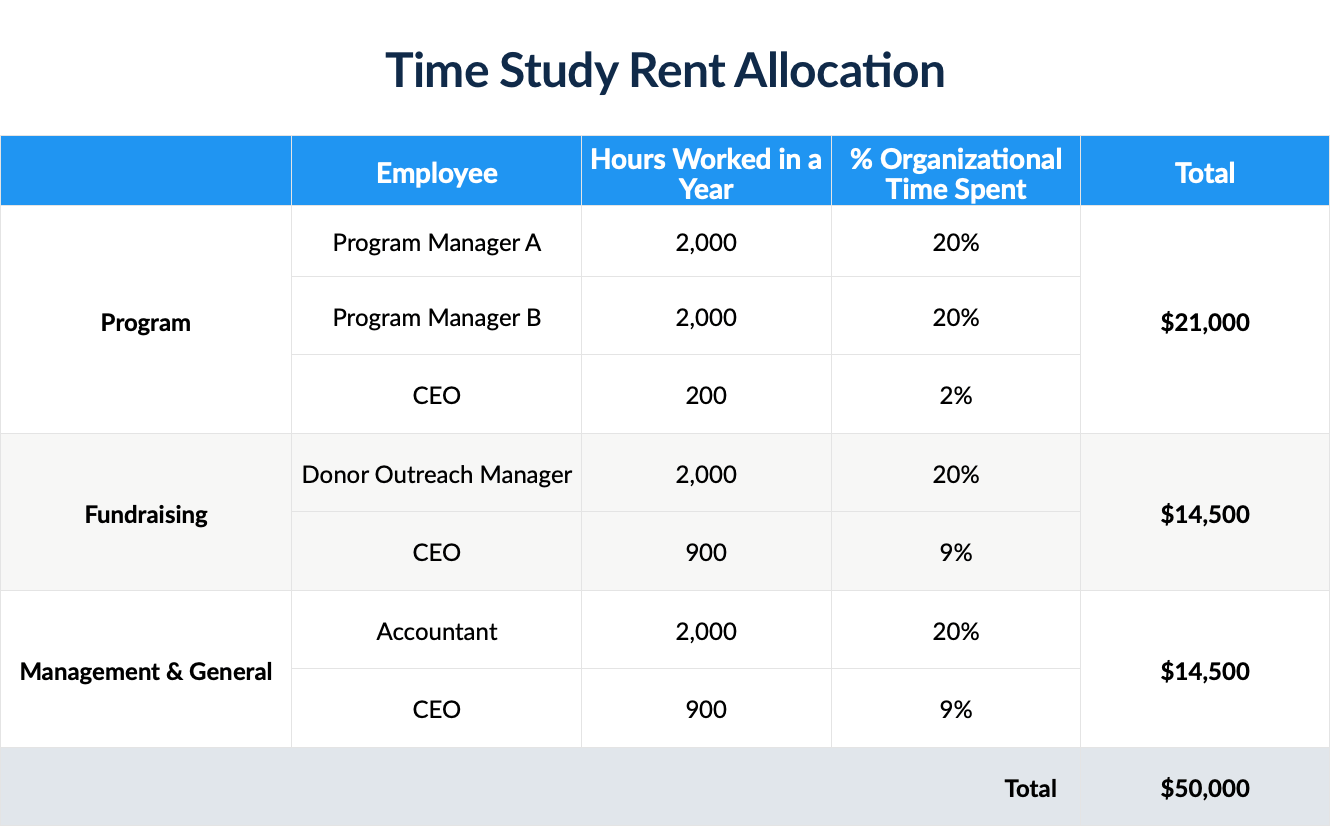

Let's say you made everyone track their time for a few months. Looking at the timesheet data, you realize the CEO actually spends about 10% of her time working directly on Program A. Using your time study findings, let's return to our rent expense ($50,000 per year) to see the difference in allocation.

With your better understanding of how your CEO spends her time, you're able to allocate $1,000 more dollars of your rent costs to program expenses, which amounts to a 2% decrease in overhead rent costs.

Why You Should Use Time Studies for Functional Expense Allocation

Making these guesses about a single employee — especially when you have some data to back you up, as we did with our CEO's hypothetical meetings calendar — is probably fine. But it doesn't give you the full picture of what's really going on in your nonprofit. And without the full picture, you'll be unable to take advantage of several benefits of the more accurate method of time study allocation.

Reducing Overhead Costs

While our example CEO was the only employee floating between functions, in most nonprofits it's common for all employees to perform multiple roles and pitch in where they're needed. So not understanding where your employees' time goes means you could potentially miss out on allocating less money to overhead expenses and more to programs.

Where this method of allocation really makes a difference, though, is with salary allocation. Payroll expenses account for about 45% to 65% of nonprofit spending. So allocating more payroll costs than necessary to fundraising and management and general classifications can add up to thousands of dollars more in overhead than you're actually spending. This is especially true for comparatively highly-paid employees, like nonprofit CEOs.

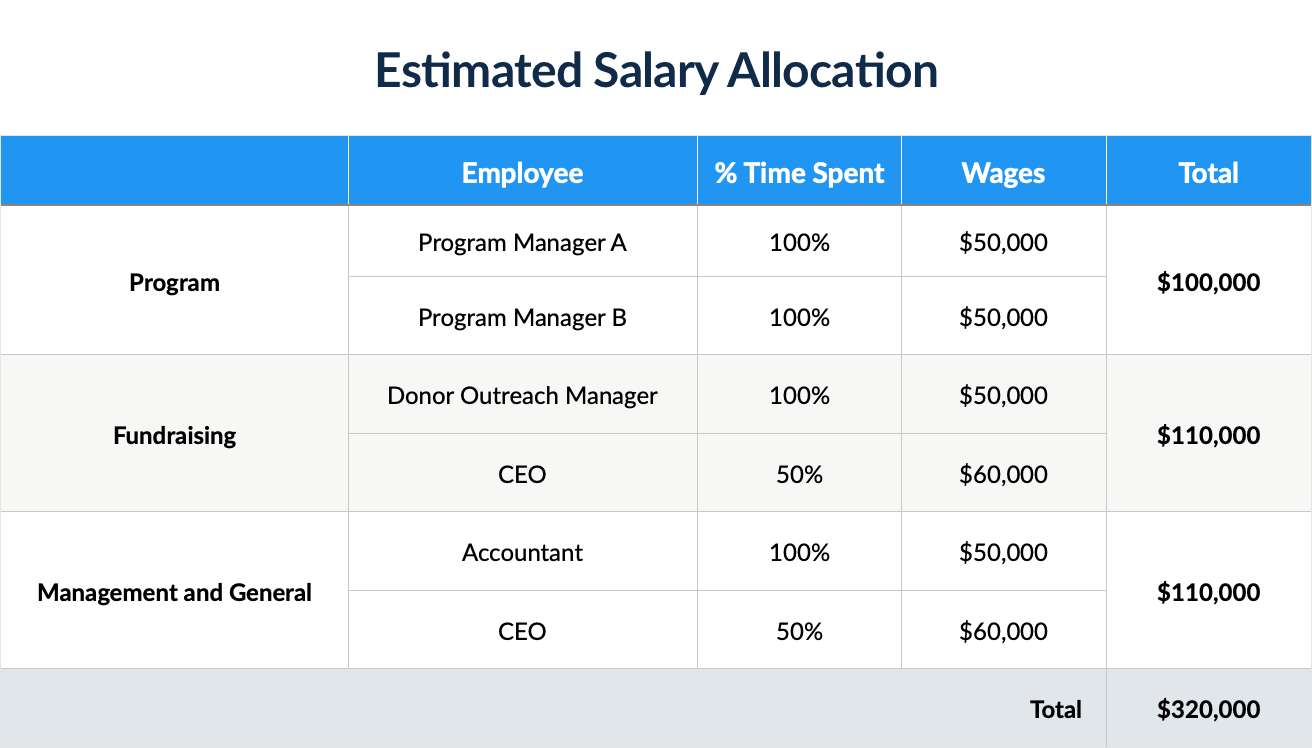

With our estimates of a CEO's time split between fundraising and management and general activities, here's what the allocations would look like.

And here's what our allocations look like when we use our time study data to show that the CEO spends 10% of her time working on Program A.

The difference in overhead costs using these two methods is $12,000 — a significant amount for a small nonprofit that needs to keep overhead low.

Maximizing Funding

That $12,000 difference is also important when it comes to allocating different types of funding.

Certain types of funding — from federal grants, as one example — stipulate that you must use their money only for certain types of expenses. And those expenses are typically limited to programmatic expenses. Most grants will typically allow you to cover a percentage of overhead costs with their funding. However, for the most part, you'll need to find other funding sources to cover fundraising and general expenses. That typically means dipping into your unrestricted funds — built up over many years of outreach campaigns — to cover these costs. With a time study, 10% of our hypothetical CEO's time — and 10% of her salary — counts as a program expense.

But here's the kicker: if we don't know our CEO spends 10% of her time on program activities before submitting a grant budget, we'll still be stuck covering that $12,000 from another funding source.

Time studies not only help you maximize grant funding by reducing your reliance on your unrestricted funds. They also help you determine how much money to ask for to cover program staff's salaries when you apply for grants.

Creating an Audit Trail

Finally, without a record of how our imaginary CEO spent her time, it's unlikely that an auditor would have believed our allocations.

Most nonprofit CEOs' time typically falls under fundraising and management and general categories. Since this CEO didn't document her time spent working directly with Program A, there would have been no easy way to prove to an auditor that 10% of her time was actually spent on programmatic activities.

Using time tracking software, you can create an audit trail for every nonprofit staff member to help auditors understand your allocation methods.

How to Do a Time Study for Your Nonprofit

Now that you understand the benefits of functional expense allocation based on time studies, you'll likely want to conduct one for your own nonprofit. And there are two main ways you could go about setting it up.

Short-Term Time Study

The easiest way to conduct a time study is to do it for a short period of time, from a pay period to several months. Using timesheet templates (since they're free and relatively easy to use), you ask employees to track their time until the time study is over. You can then use the data from this short period as a snapshot of how your organization's time is spent all year.

Unfortunately, a short-term study leaves you right where you started with other allocation methods: guessing and estimating.

Tracking time during a small window assumes that your employees' day-to-day responsibilities rarely change. And as anyone who's ever worked at a nonprofit can tell you, that's rarely the case. Especially for employees who frequently work across programs, assuming that one week will look like the next is laughable. And depending on your mission, you could have whole months that look different for your nonprofit.

What if the program our imaginary CEO spent 10% of her time on was a summer program, but you decided to conduct a time study in the fall? You might come to the conclusion that she never works on programs at all. Or what if you track time during the month before your huge annual fundraising gala? Much more staff time would be devoted to fundraising activities — and, therefore, allocated to fundraising expenses — during that time.

I could go through a million more hypothetical scenarios, but you get the point: temporary time tracking doesn't give you the full picture.

Use Time Tracking Software Every Day

If you want to experience the full benefits of time study allocation — reduced overhead, maximized funding, and audit-ready records — you have to track employee time every day. There's really no in-between.

While asking employees to fill out a timesheet every day can be a hard sell, it's the only way to gain a granular understanding of how you should allocate functional expenses. Wage allocation, especially, will be greatly impacted by requiring employees to turn in completed timesheets.

And to use timesheet data effectively, you'll want to invest in dedicated time tracking software. Unlike with spreadsheets, your employees can't accidentally alter formulas, skewing your numbers. And most time tracking tools allow managers to create notifications to automatically remind employees to submit timesheets. Software can also alert approvers to any errors, showing you where you're missing data or where an employee has made a mistake.

Finally, software, unlike spreadsheets, can create a federally-compliant audit trail. Auditors will be able to see timestamped entries and alterations, as well as hours worked to justify your functional expense allocations.

Track Employee Time to Understand How Your Nonprofit Really Spends Its Money

Understanding employee time is the key to understanding what's really happening in your nonprofit. As a nonprofit accountant, you can't follow everyone around all day trying to understand what they're really doing to get a better sense of how to allocate your functional expenses.

But employees can plug their hours into a timesheet — and maybe even include a short description of the task they worked on — to help you make smarter decisions about where your organization's money should go.

If you use time tracking software to help automate the process, you can easily pull timesheet data from the system. You can — and should — use that data for your annual return form, of course. But you can also use it to communicate transparently about spending with donors or to hand over to independent auditors who are evaluating your financial stewardship.

ClickTime's nonprofit time tracking tool makes it easy for:

- Employees to fill out completed timesheets.

- Managers to view and approve timesheets.

- Accountants to draw conclusions about spending from timesheet data.

- Auditors to understand how your nonprofit allocated functional expenses.

See how ClickTime's timesheet software can help your nonprofit create accurate functional expense statements, reduce overhead costs, maximize funding, and create compliant audit trails.